Billing cycles and interest

PayCredit offers several options for interest calculation. The system supports several variations to assist you in meeting your credit products terms and conditions and regional legislation.

PayCredit operates monthly billing cycles (also referred to as statement cycle). Debt, interest calculations and any repayments are updated during the month and at the end of the cycle a statement is produced which includes two amounts due for repayment:

- Statement Balance, i.e. the full amount of debt

- Minimum Repayment Amount

The Minimum Repayment Amount is based on a formula configured by you, typically including a % of debt, interest and fees.

The cardholder is usually provided with a grace period to repay by the repayment due date. If the full statement amount is repaid by the due date, typically interest on some of the debt is not charged.

At the end of the cycle, debt and interest calculations are carried forward to the next billing cycle.

Tracking debt (Principal)

Debt, referred to as principal, is tracked in PayCredit.

You can define different categories of debt through product configuration. These include:

- Purchases

- Cash withdrawals

- Fees

When transactions are received in PayCredit, the amounts are aggregated and added to the relevant PayCredit ledger record. In addition to the configured categories there is always a Default PayCredit ledger record.

The PayCredit ledger records are defined as part of product configuration and include setting interest rates, the APR % value, and a number of other configuration parameters.

Each billing cycle will have a PayCredit ledger record, called Product apr_id, for each debt category plus the Default. For example:

Product apr_id | Description | APR Rate % |

|---|---|---|

| 1 | Default | 20% |

| 2 | Purchases | 20% |

| 3 | Cash Withdrawals | 25% |

| 4 | Fees | 0% |

In addition to splitting debt by categories, each PayCredit ledger entry record is also divided by a time period.

- Current: debt from the current billing cycle

- Previous: debt from the last billing cycle

- Outstanding: an aggregation of all debt older than the previous billing cycle

When a repayment or other credit transaction is received, the amount is allocated as a repayment of debt. This means each record of Current, Previous and Outstanding can have a matched repayment record.

For each PayCredit ledger record, there will be the following values:

| Description of Principal | Database Field Name |

|---|---|

| Current Principal | stmnt_unpaid_principal |

| Current Principal repaid | stmnt_repaid_principal |

| Previous Principal | prev_stmnt_unpaid_principal |

| Previous Principal repaid | prev_stmnt_repaid_principal |

| Outstanding Principal | outsd_stmnt_unpaid_principal |

| Outstanding Principal repaid | outsd_stmnt_repaid_principal |

Interest calculations

PayCredit calculates accrued interest daily on principal amounts for each PayCredit ledger record.

* Accrued interest = (principal less any allocated repayment) x APR Rate % / 365 days.* The daily interest is aggregated during the billing cycle.* Interest is calculated separately for each age of debt.* Interest is accrued daily.* Interest is calculated to five decimal places and rounded to two decimal places.

After interest is calculated, there is separate logic to determine whether interest is posted to the account.

Interest only becomes a debt to be repaid once it is posted to the account.

The logic to post interest is driven by two factors:

- Always charge interest: Yes or No

- Repayment Status

Always charge interest: Yes or No

PayCredit product configuration includes setting whether or not interest is always charged for each type of debt.

Certain transactions, typically cash withdrawals or cash advances, always have interest charged from the date of the transaction. This means the grace period is not relevant for those interest amounts, even if the cardholder repays the full statement amount by the due date, interest is still posted to the account.

Purchase transactions typically do receive a grace period. This means that whilst interest is calculated it will not be posted to the account if the cardholder repays the full statement amount by the repayment due date.

Repayment Status

PayCredit tracks the repayment status of an Account.

The main driver for repayment status is whether the cardholder has repaid the last released statement by the repayment due date. The released statement will have two amounts:

- Statement balance: the full statement amount.

- Minimum repayment amount: based on a formula provided by youin the PSF.

To avoid posting interest for Always charge interest = No, the cardholder must repay the full statement amount of the last released statement.

Interest amounts to be posted

Interest is posted at the end of the billing cycle. The calculation of interest depends on whether interest is always charged on debt or not and whether the customer repays the full statement amount.

Where interest is always charged, the accrued interest from the current billing cycle together with additional calculated interest on debt from the previous or older cycles, is posted at the end of the cycle.

Where interest is not always charged, because of the grace period, the amount of posted interest is different. Accrued interest is not posted, but carried forward to the next cycle, referred to as previous accrued interest.

- If the cardholder repays the full statement amount by the due date, this interest is not posted.

- If the cardholder does not repay the full statement amount by the due date, this interest is posted, together with new calculated interest interest on the carried forward debt

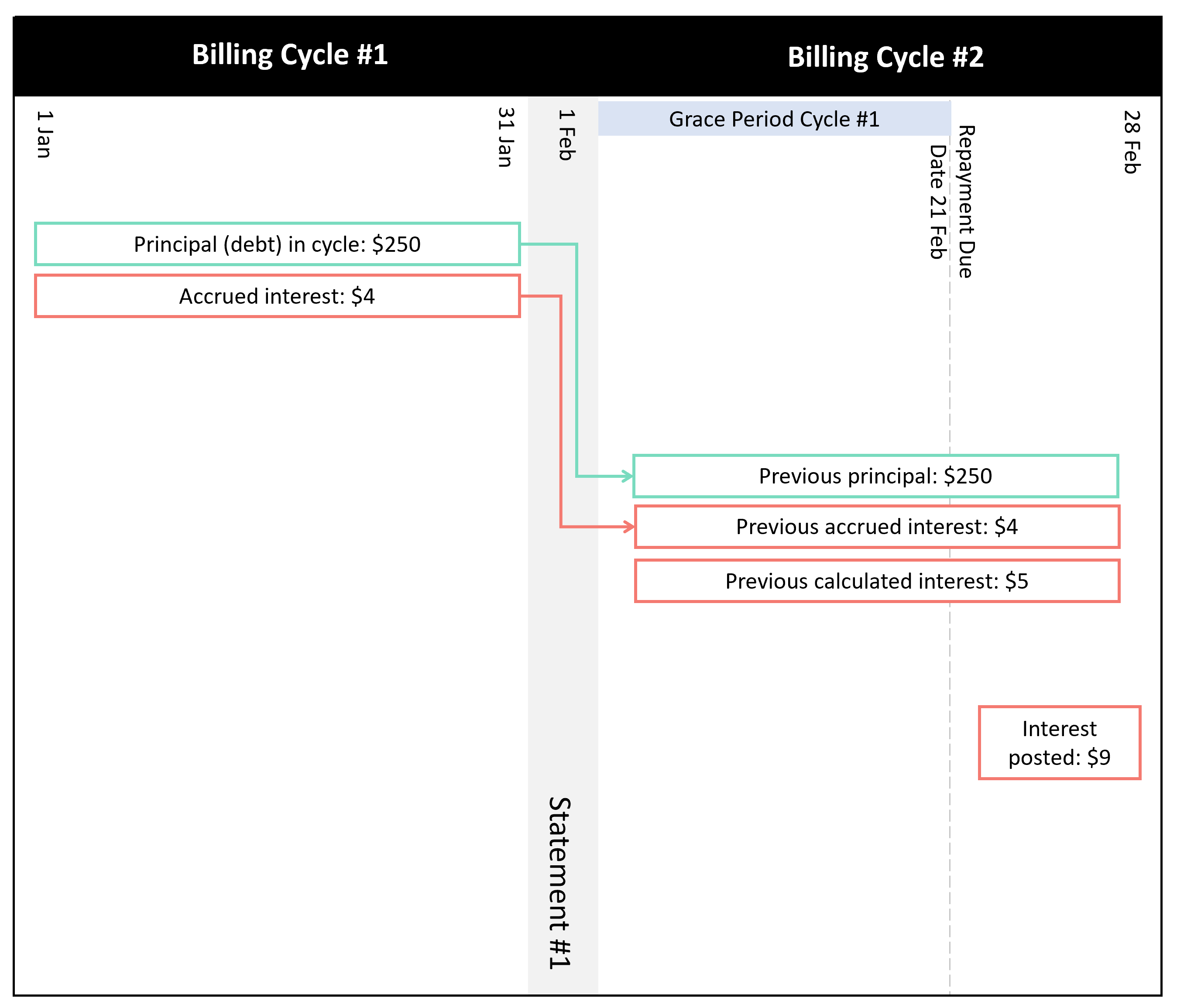

PayCredit billing cycle example

Simplified example of PayCredit billing cycle

In this example (Simplified example of PayCredit billing cycle):

- Debt (referred to as principal) is recorded across the month of January with daily accrued interest.

- At the end of the cycle a statement is released on 1st February, with total debt of $250.

- Total accrued interest during January is $4, but the interest is not included in the statement. The customer has the grace period to repay the $250, if the full amount is repaid no interest is charged.

- The principal of $250 from the January cycle and the accrued interest for January of $4 is carried forward to the next cycle, referred to now as ‘previous principal' and ‘previous accrued interest'.

- Daily accrued interest continues to be calculated during February on the previous principal, referred to as ‘previous calculated interest’.

- If the full statement amount of $250 is repaid by the repayment due date of 21 February, no interest is charged.

- If repayment is less than full statement, then interest is posted to the account at the end of the cycle, end of February. Posted interest is both previous accrued interest from the January cycle of $4 and the previous calculated interest, $5 that has accrued during February.

- At the end of cycle #2 total posted interest is $9.

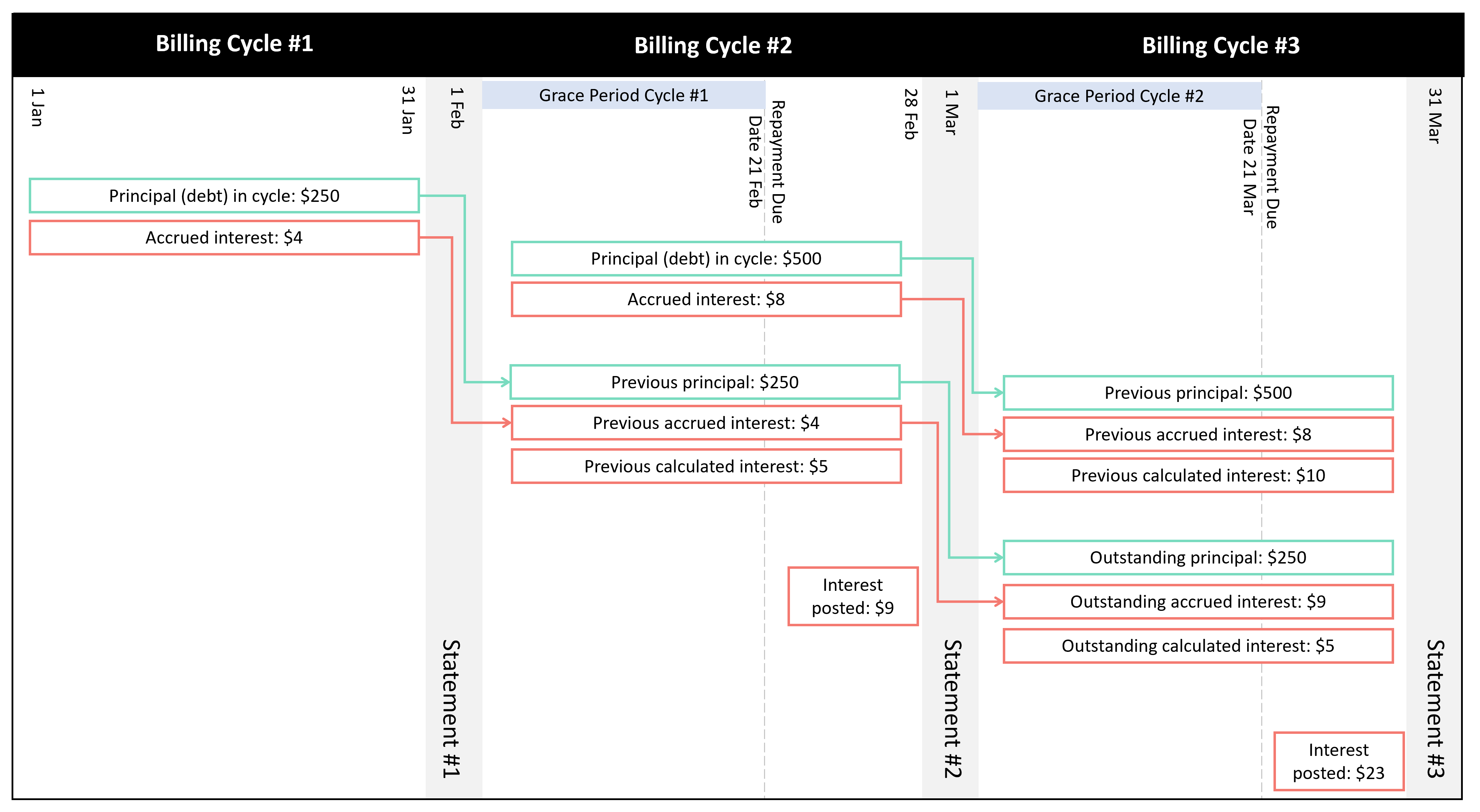

Simplified example of PayCredit billing cycle #2

In this example (Simplified example of PayCredit billing cycle #2):

- The previous principal amount from February is carried forward to the March cycle, now referred to as outstanding principal.

- The posted interest in February (which is total of previous accrued interest + previous calculated interest) is carried forward to the March cycle as a combined value, now referred to as outstanding accrued interest.

- Daily accrued interest continues to be calculated during March on the outstanding principal, referred to as ‘outstanding calculated interest’.

- In any statement cycle, there is likely to be principal and interest calculations for current, previous and outstanding amounts.

- In the example below, at the end of the March cycle #3, the total posted interest is $23 including:

- Previous accrued interest from February: $8

- Previous calculated interest during March: $10

- Outstanding calculated interest during March: $5

- The outstanding accrued interest of $9 has already been posted to the account, but is still tracked in the system until it is repaid.

Updated 10 months ago